New Risks to Growth

A new war in the Middle East complicates India's geopolitics and poses new risks to domestic growth

Political & Policy Issues to Watch

The Iran war has upturned a fragile balance

The outbreak of a full-blown Iran-US-Israel war has further complicated India’s already-delicate geopolitical calculus, as well as its domestic politics. Through its silence, and a recent state visit to Israel by PM Modi, New Delhi has clearly signalled a tilt towards the US-Israel camp, departing from its more traditional ‘non/multi-aligned’ posture. Together with the recent rapprochement over trade with Donald Trump, this has opened up space for India to resume oil imports from Russia, albeit temporarily. However, it has also left room for the Opposition to target the Modi government for supposedly 'selling out'. This could impact some of the tighter races in upcoming state elections in Assam, Kerala, West Bengal, Tamil Nadu and Puducherry.

Legislative progress has been grindingly slow

The West Asia situation will cast a deep shadow over the ongoing Budget Session of Parliament, which has so far proven rancorous and unproductive. Repeated disruptions, a planned non-confidence motion against the Speaker and possible impeachment proceedings against the Chief Election Commissioner have all helped ensure that few bills get discussed, let alone passed. So far, just one piece of legislation – the Industrial Relations Code (Amendment) Bill – has got through. From all indications, the government may content itself with passing the Finance Bill, or possibly drive through amendments to the Electricity and Insolvency and Bankruptcy Code Acts.

View interactive version: https://datawrapper.dwcdn.net/GOSho/1/

View interactive version: https://datawrapper.dwcdn.net/UwUGq/2/

Outlook for the Market

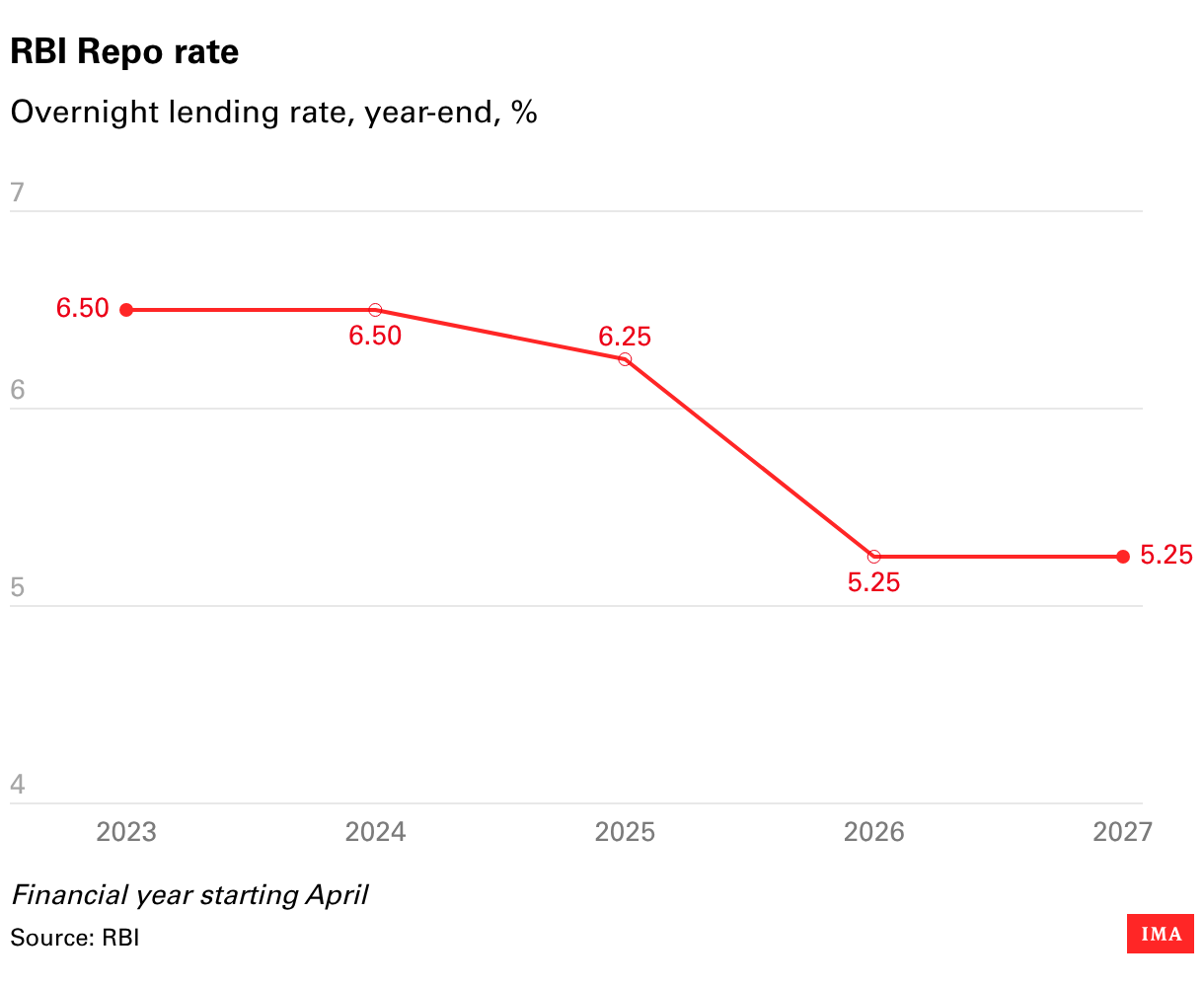

View interactive version: https://datawrapper.dwcdn.net/O6I1W/1/

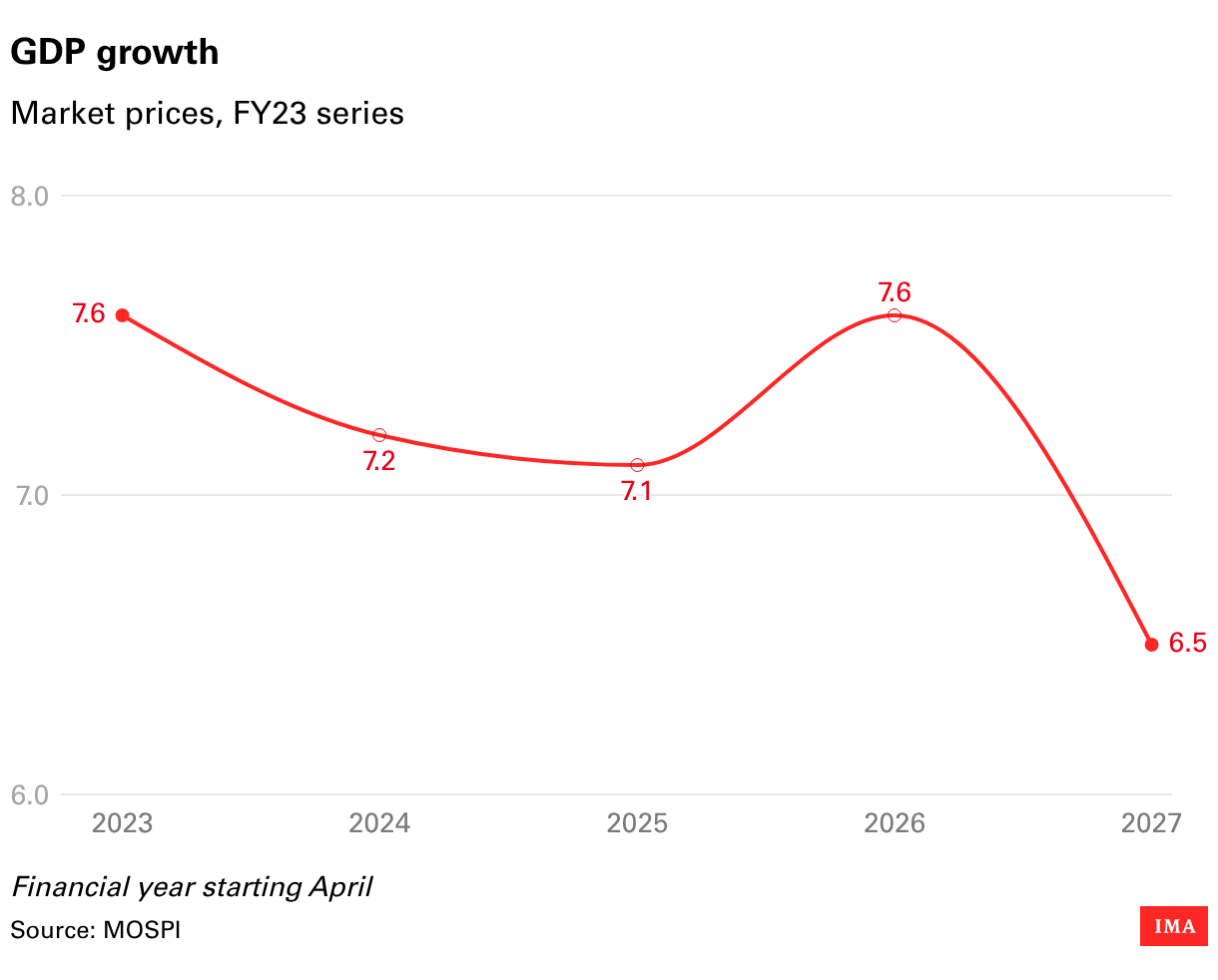

A new GDP series, (almost) same growth story

India’s newly-released, 2022-23 base GDP series offers welcome refinements to the methodology behind the growth numbers. It better captures activity in the informal sector, leans more heavily on robust datasets (e.g. GST receipts) and fixes certain issues around deflation/extrapolation. On net, though, the Indian economy is now estimated to be slightly (3-4%) smaller than previously thought, tilted less towards services (~53% vs >55%) and private consumption, but more towards agriculture (21%). These findings may be relevant to medium-term businesses planning.

Risks ahead…

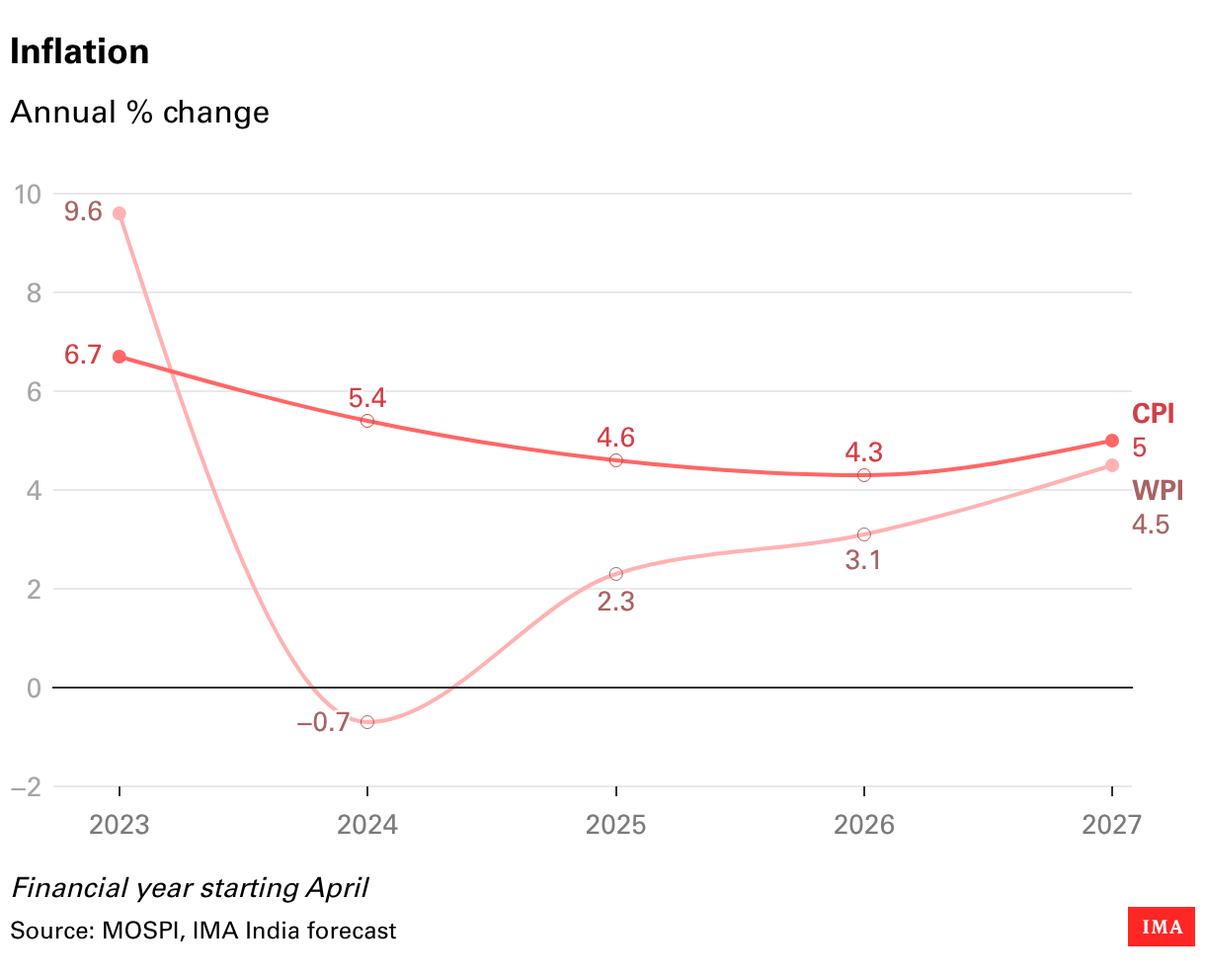

For now, the lead indicators remain strong. The February PMIs for Services (58.1, slightly down from 58.5 MoM) and Manufacturing (56.9, up from 55.4) remain above-trend. GST receipts (Rs 1.84 trillion) and e-Way bill issuances (137 million) are holding firm. Exports grew marginally (0.6%) in January but imports jumped 19%, causing the trade balance to widen. Meanwhile, going by India’s new-and-improved (2024 base) CPI numbers, inflation stood at a mild 2.75% in January, though this was markedly higher than December’s value of 1.3% (using the old series). Finally, auto sales continued to surge in February, with passenger vehicles, two-wheelers and commercial vehicles all rising by over 25%.

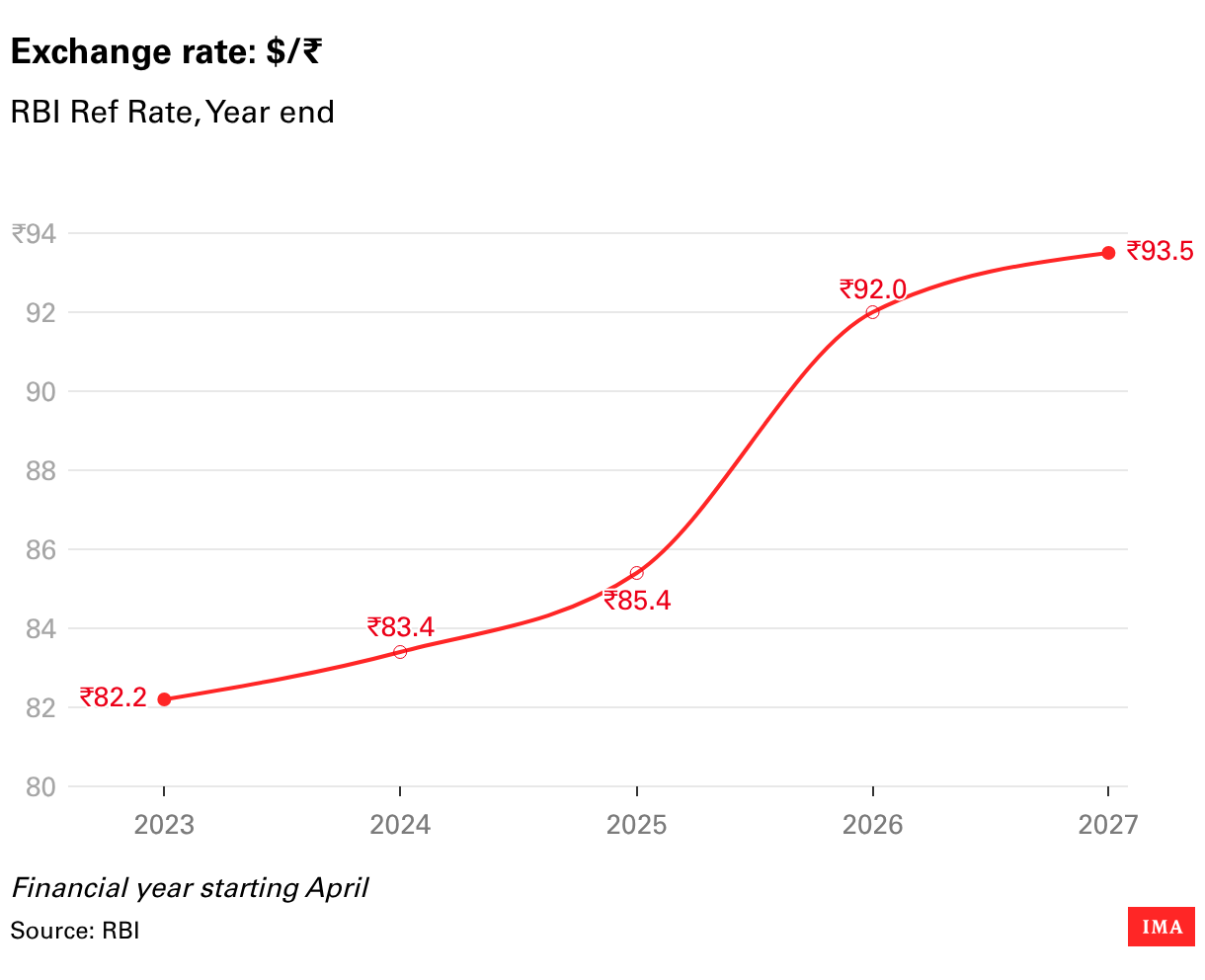

Depending on the course of the war, the coming months may not look as benign. Early March saw financial markets plunge, the rupee slide past 92/$ and FII flows turn negative again. Should the situation fail to resolve, the pressures on inflation, the trade and current accounts, the Indian currency, and eventually, consumption (including through a negative wealth effect) and growth could intensify. The coming weeks will prove crucial in this regard.

View interactive version: https://datawrapper.dwcdn.net/QECpc/2/