Scaling D2C in India

Building Consumer Brands in the Digital Economy

Executive Summary

Together, cheap data and the UPI payments system have made online discovery the default starting point for Indian consumers.

D2C is now a solid brand-building route, with scale coming from offline expansion.

Tier-2/3 shoppers are driving growth, making visibility and trust more important than distribution reach.

Quick-commerce and marketplaces have become high-value digital shelves, reshaping how brands win visibility.

Omnichannel strategies have become essential, with offline stores and quick-commerce improving conversion and lowering CAC.

India’s digital economy has been transformed by one fundamental shift: a collapse in the price of data. A gigabyte, once ₹200, now costs less than ₹9, bringing the internet to more than 800 million users, including across Tier-3 and Tier-4 towns. Combined with rising incomes and frictionless payments – the UPI system processed over 20.7 bn transactions worth ₹27.28 tn in October 2025 – this has created the rails for one of the world’s most dynamic e-Commerce ecosystems.

Within this landscape, Direct-to-Consumer (D2C) brands have moved from niche to mainstream. e-Commerce has lowered entry barriers, enabled national reach and provided powerful digital rails for discovery and payments, fuelling the rise of hundreds of new consumer brands. The narrative is not about online replacing offline. It is about digital foundations eventually supporting an omnichannel model. Most brands begin online to validate products and build early traction, then expand offline through exclusive stores, modern retail partnerships and q-Commerce placement. Digital discovery and first-party data remain the engine of the model, while offline channels add scale, trust and more durable customer stickiness.

The Structural Drivers of D2C Growth

Consumer demand: Digital-first shopping at scale

India now has the world’s 2nd-largest base of online shoppers. Tier-2/3 cities are driving much of this growth, and consumers are experimenting with previously inaccessible brands. Digital discovery has removed distribution bottlenecks and ‘online’ has negated physical shelf space as a constraint.

Payment infrastructure: Smooth and trusted transactions

UPI now accounts for over 83% of digital transactions in India. Zero-cost and real-time payments reduce friction in the buying journey, which encourages trial purchases. This is especially important for early-stage D2C brands that rely on impulse and experimentation.

Distribution platforms: From marketplaces to networks

Marketplaces such as Amazon, Flipkart and Nykaa continue to offer scale advantages, but rising advertising costs are reducing their margins. The government-led ONDC (open network for digital commerce) offers a competing model, but adoption remains uneven. Quick-commerce platforms such as Blinkit, Instamart and Zepto are now both, storefronts and high-value advertising spaces. Placement with them is a new form of ‘digital shelf’, especially in beauty, snacks and personal care.

Data regulation: Compliance as strategy

The Digital Personal Data Protection (DPDP) Act of 2023 has introduced stricter rules for consent and usage. Compliance costs have increased, but the long-term winners will be brands that build strong first-party data ecosystems using loyalty programs and omnichannel integration. Clean and consent-driven data has become a foundation for personalisation and retention.

Market Trajectory and Investment Flows

Even as India’s D2C market has firmly entered the mainstream, since definitions vary, so do market-size estimates. Bain placed e-Retail as a whole at about $60 bn in 2024 while Mordor Intelligence expects the D2C e-Commerce segment alone to reach $87.5 bn this year and about $267 bn by 2030. The range reflects how dynamic and fast-evolving the sector truly is. Investor interest remains strong. Between 2020 and 2023, D2C brands in India raised more than $4 bn across 730 deals. Valuations have normalised post-Covid, but capital continues to flow to brands that demonstrate healthy unit economics and a clear path to profitability. The focus has shifted from gross merchandise value to efficiency and retention.

View interactive version: https://datawrapper.dwcdn.net/4zvPA/2/

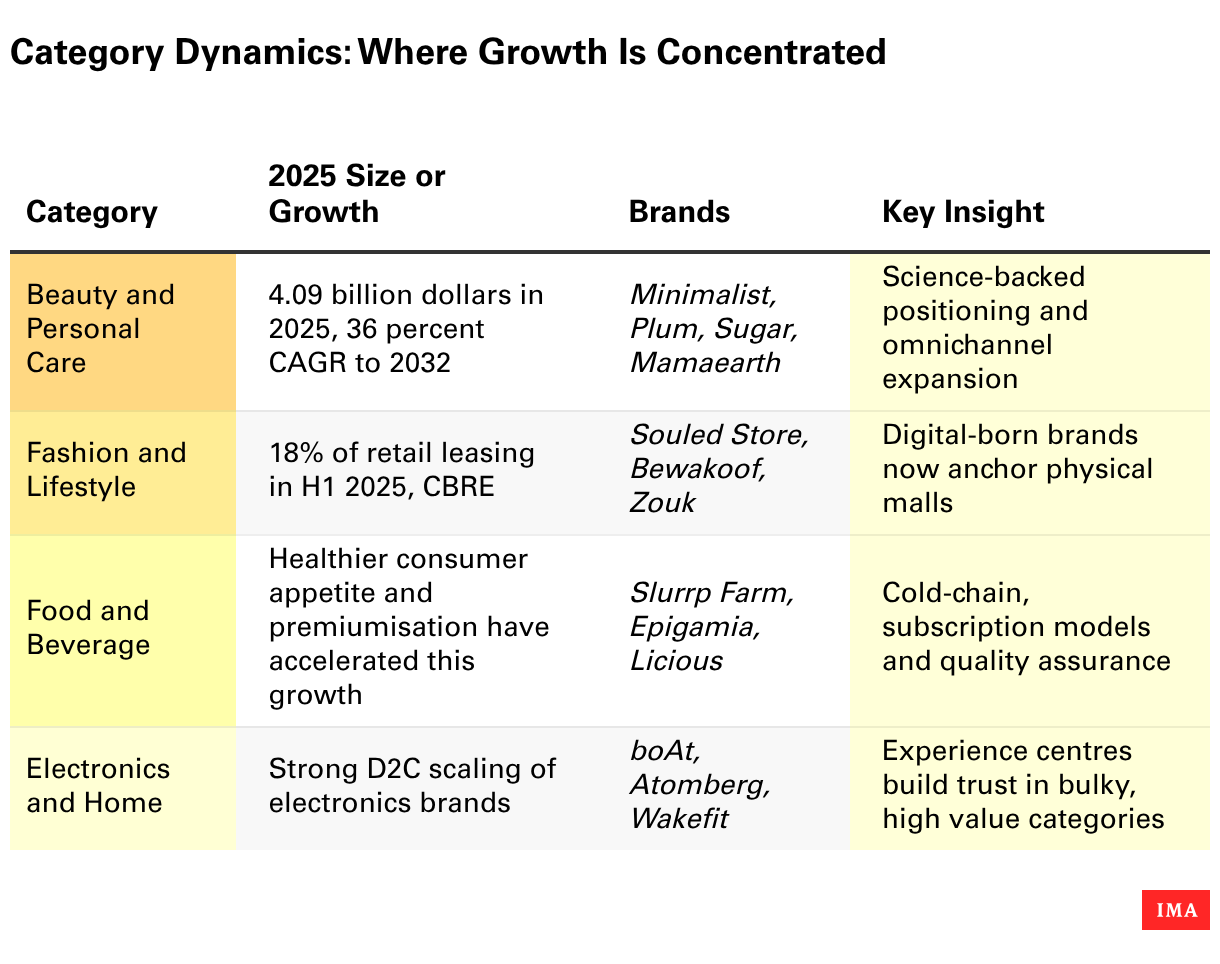

Case Studies: Success and Strain

Mamaearth: mass visibility through retail reach. Starting out as a toxin-free baby brand, Mamaearth now spans multiple beauty categories and is targeting over 150,000 retail outlets. Online validation enables trust, while offline presence ensures ubiquity.

Wakefit: omnichannel trust in furniture. Wakefit pioneered the mattress-in-a-box segment, built its own logistics and opened experience centres. Now preparing for an IPO, it has proven that even bulky, trust-sensitive categories can scale digitally if supported by selective offline anchors.

The Souled Store: community and culture as differentiation. Leveraging pop-culture licences and community engagement, The Souled Store recently turned profitable, with ₹3.6 bn in revenue. Offline expansion is consolidating its base, showing how community-driven differentiation sustains profitability.

boAt: the challenge of commoditisation. boAt achieved scale through affordable, stylish audio products, but category commoditisation and global competition have slowed its growth. Its experience illustrates the need for defensible moats beyond price and influencer marketing.

Minimalist and GIVA: insurgents to watch. Minimalist has built rapid traction in skincare through science-based positioning. Meanwhile, GIVA’s inroads into the jewellery segment demonstrates how D2C can expand into non-traditional verticals beyond beauty/fashion.

The New Economics of D2C

The original D2C model relied on performance marketing and rapid scale, but this model is now under pressure. Customer acquisition costs (CAC) have risen sharply as digital advertising matures. Marketplace visibility requires expensive sponsored listings. q-Commerce platforms now charge premium rates for in-app placement. High return rates in beauty and fashion continue to erode contribution margins. Offline channels, despite higher upfront costs, help reduce CAC, build trust and bring down return rates through trial. Investors are rewarding brands that prioritise retention, contribution margins and disciplined expansion, rather than pure growth.

The Omnichannel Pivot

Despite their digital DNA, D2C brands are increasingly embracing offline. CBRE reports that D2C brands leased nearly 600,000 sq ft of retail space in H1 2025, more than double the year before, with fashion alone accounting for 60%. Offline stores are no longer seen as optional; they are essential to reducing CAC, deepening trust and providing experiential value. q-Commerce, meanwhile, is serving as both trial engine and advertising channel, with categories such as beauty and snacks using placements on these apps as intensively as they did with TV commercials a decade ago. Plainly, then, offline is not the opposite of D2C but its natural next stage. Digital builds the engine, while offline provides scale and sustainability.

Strategic Implications for CXOs

Choose the right strategic pathway. Large companies can build their own D2C brands, partner with promising insurgents or acquire high-potential players for integration.

Design channel architecture deliberately. Online channels shape discovery and loyalty. Offline channels provide trust and lower acquisition costs. Marketplaces deliver reach, but margins remain under pressure. q-Commerce enables immediacy and experimentation.

Treat data as a long-term moat. Under the DPDP Act, clean and consent-driven data collection through loyalty programs and apps is both a compliance requirement and a competitive advantage.

Align growth with profitability. The market values sustainability over pure scale. Retention, contribution margins and community strength matter as much as absolute GMV.

The evolution of D2C in India is not a story of digital brands replacing incumbents. It is about the rewiring of retail itself. Consumers do not think in terms of channels. They expect speed, personalisation and convenience, whether they shop through an app, a marketplace or a physical store. Brands that combine digital intimacy, omnichannel execution and financial discipline will define the next chapter of India’s consumer economy.