Will the Smartphone Survive the Next Decade?

Three scenarios for 2036

Executive Summary

The smartphone is unlikely to disappear by 2035, but it may lose its control over the first moment of consumer intent.

Its dominance came from bundling discovery, identity, payments and commerce into one surface. The next decade will test whether that bundle holds.

Three futures are plausible: the smartphone's dominance persists; primacy shifts to a higher interface layer; or the phone becomes secondary.

Structural inertia is strong, supported by billions of mobile subscribers and entrenched ecosystems.

AI-mediated interaction and alternative surfaces are already scaling.

Each of the previous few decades have been defined by an interface that controls access to information, attention and transactions. The 1990s belonged to the PC. The 2000s belonged to the internet browser. The 2010s belonged to the smartphone.

The smartphone’s true achievement was not hardware. It was control over attention and distribution. It became the storefront, the billboard, the wallet, the camera, the remote control and the identity card, compressed into a single object. Entire industries reorganised themselves around the assumption that the smartphone is where discovery begins, persuasion occurs and (if luck is by their side) transactions close.

Yet, the coming decade may see a rare transition. The smartphone may not be killed, but increasingly, competition will increasingly be about which interface owns the first moment of intent. Phones will compete not only with other phones, but with experiences that feel faster and more natural across voice assistants, wearables, cars, TVs and ambient devices. This shift will cascade into software. Apps will contest for installs, and for being the default execution partner across interfaces.

In that world, the smartphone will still matter, but the battleground will move away from the home screen and toward the mechanisms that decide what gets recommended and what gets executed.

The Three Futures

Is the smartphone on the verge of extinction? Or is it on the verge of losing its monopoly over consumer attention and choice? That distinction matters. The interface might stop being the default starting point for intent, and distribution models may reset. At its core, the smartphone is a bundle. The next decade will decide whether that bundle survives. This is less about ‘What replaces the phone’ than about ‘What sits above it.’

To map this transition, we outline three scenarios for 2036, showing how the smartphone’s role could remain intact or be structurally diminished without disappearing.

Scenario 1: The Smartphone Stays King

There's a reason why paper isn't obsolete, despite having been around for hundreds of years. It continues to offer immense utility, particularly as a tabula rasa that can store or display information; one that's flat, maximises surface area, minimises weight and is perfect for visual and tactile creatures like us. The modern smartphone compares in this form factor.

Should the smartphone remain the main surface for digital life in the future, AI will become a key feature inside the phone, enhancing its productivity, summarisation and personalisation capabilities (not to mention its photo-taking abilities), but consumer behaviour will continue to revolve around tapping, scrolling and app ecosystems.

The scale of mobile penetration reinforces this durability. According to GSMA Intelligence, there are approximately 5.8 billion unique mobile subscribers globally, underscoring the near-universal embedment of mobile connectivity. Within that ecosystem, smartphones remain the primary access device. Counterpoint Research’s Smartphone Installed Base Tracker shows that Apple and Samsung have each surpassed one billion active devices in circulation, together accounting for roughly 44% of the global active installed base. Such ecosystem depth, platform familiarity and behavioural habit create significant structural inertia.

Implications for Business

If the smartphone retains its dominance, today's core rules/behaviours will largely persist.

App distribution and store visibility will remain the primary competitive levers.

Performance marketing and in-app personalisation will continue to drive growth.

First-party data within app ecosystems will retain strategic value.

AI investment will focus on enhancing existing mobile journeys rather than redesigning interfaces.

In this world, optimisation will outperform reinvention.

Scenario 2 (Base Case): The Smartphone as the Hub, not the Surface

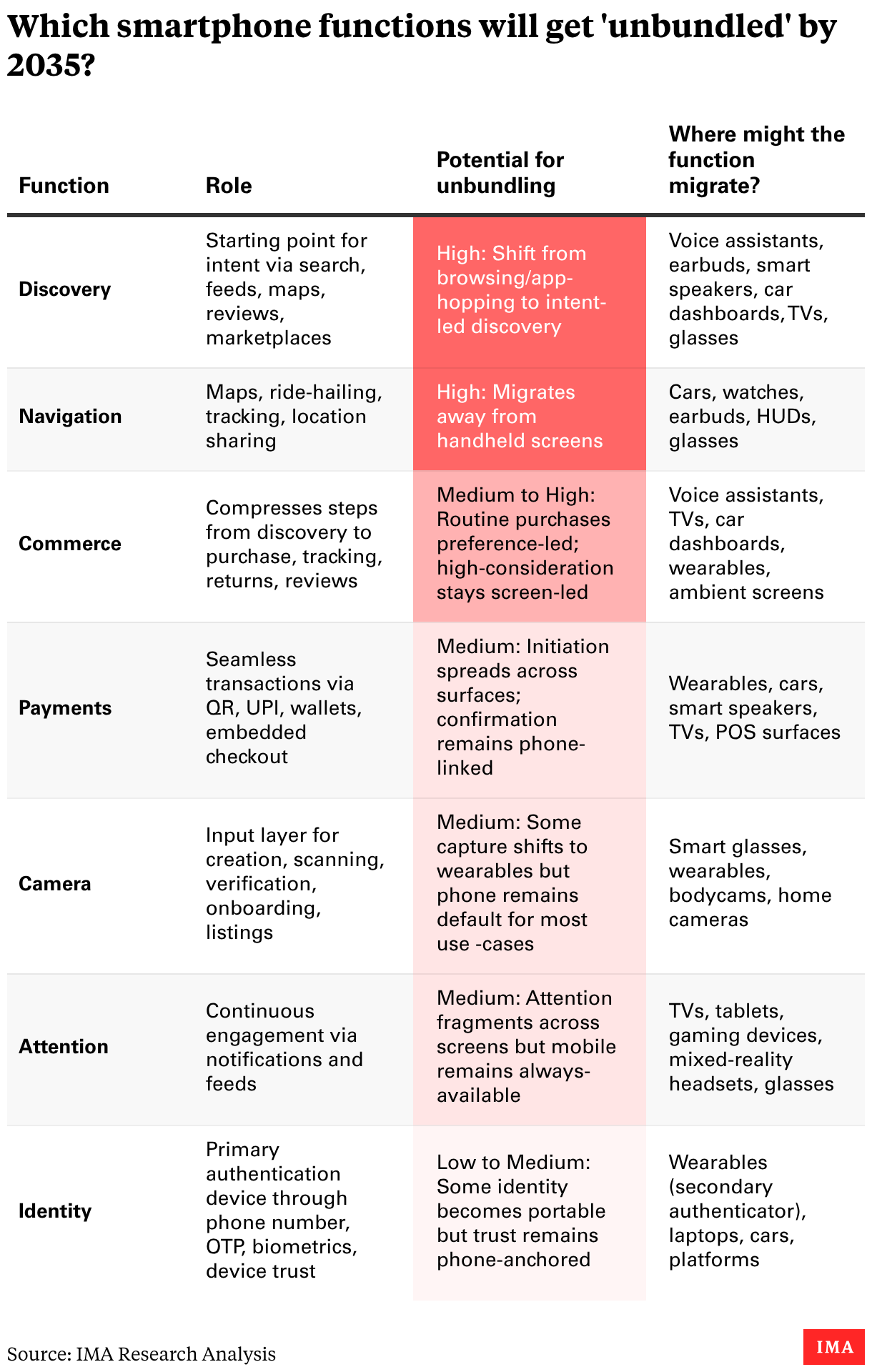

This is the most plausible future for 2036, given that the main risk to the modern smartphone is interface unbundling. The smartphone’s dominance comes from a simple but under-appreciated advantage. It did not win because it was a better phone. It won because it merged multiple critical functions into a single always-available interface. It became the default gateway through which consumers discovered information, built trust, authenticated themselves and completed transactions.

One way to understand the smartphone’s dominance is to view it as a bundle of functions that were previously segregated. The question for the next decade is which parts of that bundle remain phone-centric, and which parts detach and migrate to other devices and surfaces.

For most of the last decade, the smartphone’s power came from bundling all these roles into one interface. The next decade may be defined by the opposite dynamic. The smartphone is unlikely to disappear, but it may no longer monopolise these roles. Several functions the phone once owned end-to-end are beginning to detach and migrate to other surfaces and layers. This is the beginning of the unbundling.

View interactive version: https://datawrapper.dwcdn.net/eMRt0/3/

In this world, the smartphone remains in the pocket, but interaction shifts upward, into a layer that sits above apps, distributed across earbuds (voice), watches (glances), cars and TVs (ambient screens) and eventually lightweight glasses. Phones will become the identity, compute and payments anchor, but it will stop being the place where most discovery and decision-making begins. Indicatively, Gartner’s 2025 forecast suggests that mobile app usage could be roughly 25% lower by 2027 as AI assistants increasingly mediate user interaction.

The defining change here is not hardware but the emergence of AI assistants and agents as the organising layer of consumer intent. This idea has been articulated by major platform leaders for years. In a Microsoft Ignite keynote, Satya Nadella described the personal digital assistant as a new run-time and organising layer mediating access to applications and information across devices. More recently, he has spoken about multi-agent orchestration across applications.

The market signals are also visible. Wearables are scaling into mainstream interface territory. Canalys reported that global wearable band shipments grew 13% YoY in Q1 2025, signalling sustained adoption beyond early adopters. Meanwhile, platform economics are shifting toward services and cross-device layers. Apple’s FY2025 10-K shows Services net sales of $109.2 bn alongside iPhone at $209.6 bn. This is consistent with a world where value increasingly sits in the layer above the device.

Implications for Business

If interaction shifts upward into an interface layer, distribution economics will reset:

Being surfaced by recommendation engines will matter more than app installs.

API readiness and machine-readable systems will become strategic infrastructure.

Default fulfilment status will become more valuable than app share.

Trust, identity and structured data will be core competitive assets.

Here, brands will compete to be selected, not browsed.

Scenario 3: The Smartphone as a Legacy Device

In the third scenario, the smartphone still exists but becomes secondary, used occasionally like many laptops are today. Daily digital life will shift to other surfaces, so navigation, messaging, discovery and routine purchases will no longer require pulling out a phone.

For this to materialise, multiple constraints must break at once: Comfort, battery life, privacy, social acceptability, and interaction that feels natural in public. Still, the strategic intent has become explicit. Meta has unveiled an AR glasses prototype (Orion), positioning it as part of a long-term ambition to build an AI-centric device that could replace smartphones.

The most plausible pathway begins with wearables, which may diversify, not just improve. Apple’s AirPods Pro 3 include a heart-rate sensing feature, and smartwatches have already moved beyond notifications into health tracking and payments. If hearing devices can stream content, translate in real time and act as an always-on interface, how long before the phone becomes optional for many daily tasks? Watches could themselves evolve into bracelets and cuffs with better interfaces and longer battery life. Once those surfaces become robust, there is less need for a phone as a distinct object.

From there, entirely new categories can emerge. What if ‘home’ becomes a computing surface? Virtual windows, wall displays and always-on screens could take off as collaboration and entertainment continue moving to larger environments. Products like Google Beam hint at what this could look like. The leap from Ray-Ban Meta smart glasses to contact lenses that monitor health, enhance vision and digitally capture moments may sound extreme today, but the direction is clear: more computing will move onto the body and more interaction will become ambient. Cybernetic interfaces like Neuralink are unlikely to gain mainstream consumer trust within a decade, but they signal where the frontier is moving.

In this scenario, the smartphone will not disappear. Rather, it will become what the PC is today: still useful, but no longer the default.

Implications for Business

If interaction migrates to wearables and ambient surfaces, attention will fragment and the current interface assumptions will break:

Screen-first design will weaken while voice, glance and gestures will gain importance.

Brand equity will matters more where comparison surfaces shrink.

Hardware partnerships and ecosystem alliances will become strategic hedges.

Selective long-term bets in spatial and ambient computing will become rational portfolio options.

In this world, surface control replaces screen control.

What the Signals Collectively Suggest

The most likely scenario (number 2) is one where phones will not disappear, but their usage will see subtle yet profound shifts. The centre of gravity will migrate, with phones retaining their centrality as a hub while losing interface primacy. Across all three scenarios, though, the most consistent directional change is the rise of an interface layer that increasingly mediates choice. That is the strategic discontinuity that businesses face: In a world where consumers ask an assistant to pick, compare, book, reorder, return and recommend, the competitive battleground will move away from app installs and UI flows toward being the default option surfaced by the interface.